You Have the Money. The Officer Doesn't Believe You.

You've saved for years. You meet the threshold. You have more than enough in the bank. And your visa gets refused — not because you lacked the funds, but because of how you showed them. A single large deposit three weeks before your application. A bank statement printed from a portal instead of stamped at the branch. An average balance that dipped below the minimum on day 14 of a 28-day window you didn't know existed. The money was always there. The documentation said otherwise.

This happens constantly, and it happens to people who did their research. You read the government website. It told you the number — $15,263 for a single applicant to Canada, £13,761 for a London student in the UK, €11,904 for a German blocked account. You hit the number. What the government website didn't tell you is that the number is the beginning of the assessment, not the end of it. The officer isn't just checking whether you have the money. They're checking where it came from, how long it's been there, who controls it, and whether the transaction pattern on your statements looks like someone who genuinely has these resources — or someone who borrowed them for the application and plans to return them next week.

So you go to Reddit. One thread says three months of statements is enough. Another says six. A YouTube video explains the UK's 28-day rule but gets the closing date wrong — and if you follow that advice, your funds will show 33 days before your application instead of 31, and UKVI will reject it as out of window. An immigration lawyer's blog from 2023 quotes the old Canadian settlement fund thresholds. A forum post confidently explains that you can use your uncle's bank account for a UK student visa — you can't. Only a parent or legal guardian's account is accepted, and using anyone else's means an automatic refusal.

The free information exists. It's also fragmented across dozens of sources, frequently wrong, and never organized by the country-specific rules that actually determine whether your documentation passes or fails. Meanwhile, your application fees, language test scores, medical exams, and credential evaluations have already cost you somewhere between $2,700 and $11,400. The financial documentation is the last piece — and it's the piece where a formatting error or a timing miscalculation can invalidate everything you've already spent.

Here's what the government portals never explain: immigration officers don't just verify bank balances. They conduct forensic pattern analysis on your financial history. They're trained to detect "fund parking" — the practice of borrowing money to inflate your balance before applying and returning it afterward. A sudden deposit of $20,000 into an account that normally holds $2,000 isn't proof of funds. It's a red flag that triggers a Request for Evidence or an outright refusal, even when the money is legitimately yours. Officers at high-volume consulates in Lagos, Mumbai, and Islamabad see this pattern hundreds of times per week. They know what borrowed money looks like, and they know what genuine savings look like. The difference isn't the amount. It's the trail.

The Financial Documentation & Proof of Funds Guide is built around the Forensic Compliance System — a country-by-country framework that maps exactly what each immigration authority examines beyond the headline number: the transaction patterns they flag, the statement formats they accept, the timing windows they enforce, and the sourcing documentation that turns a suspicious deposit into a verified transfer. Not a threshold list. Not a blog post summary. A system for making your financial reality legible to the officer reviewing your file.

When your documentation tells the same story your bank balance does, the financial assessment stops being a trap and becomes a formality. The funds are yours. This makes sure the officer sees it.

Start with the free Quick-Start Checklist — a document readiness audit you can run tonight to identify gaps in your financial evidence before they become refusal reasons. Or keep reading to see what the full guide covers.

What's Inside the Forensic Compliance System

A multi-chapter guide, a quick-start checklist, and a standalone red flag toolkit. Everything structured around one principle: having money and proving money are two different skills, and the second one has country-specific rules that change every year. Whether your application is due in six weeks or six days, the framework scales — start with your destination country's chapter, then work outward.

Understanding Proof of Funds (Chapter 1)

The anatomy of a financial refusal — what officers actually write in their notes, what "insufficient proof" means when you clearly have the money, and the three pillars of financial verification: availability, transferability, and unencumbered ownership. Every immigration authority evaluates financial documentation on these dimensions — liquidity (can you access it immediately), consistency (does the balance match your income pattern), sourcing (where did it come from), and control (whose name is on the account). This chapter teaches you to audit your own finances through the officer's lens before you touch a single bank statement.

Country-Specific Requirements

Canada — Settlement Funds, GICs, and the Six-Month Average (Chapter 2)

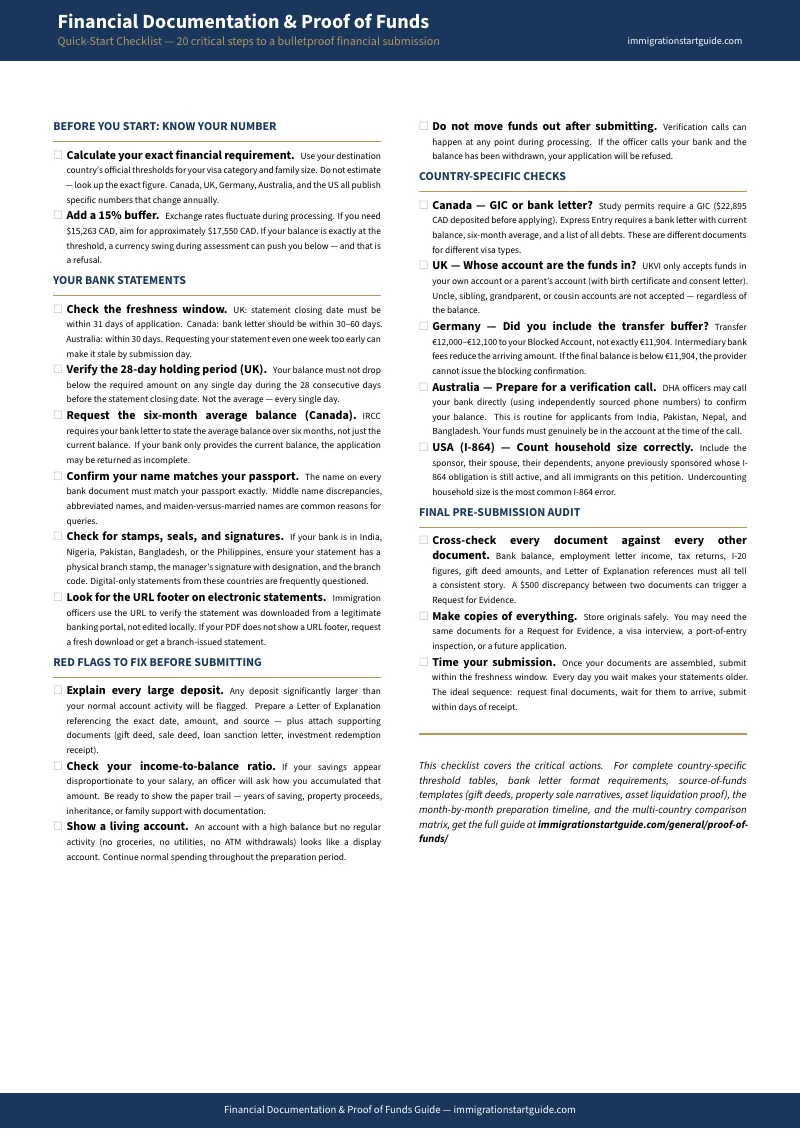

IRCC doesn't just check your current balance. They require a bank letter on institutional letterhead showing your average balance over six months, all outstanding debts, and the institution's contact details. If your bank only prints the current balance — which many banks outside North America do by default — your application comes back incomplete. The chapter covers Express Entry settlement fund thresholds by family size, the $22,895 GIC requirement for study permits, what "unencumbered" actually means in IRCC's definition, and the specific bank letter format that satisfies federal requirements. Plus the Provincial Nominee Program variations that layer additional requirements on top.

United Kingdom — The 28-Day Rule and Appendix Finance (Chapter 3)

The UK system is the most technically rigid. Funds must be held for 28 consecutive days in a regulated financial institution, and the end of that 28-day period must fall within 31 days of your application date. If the balance dips below the threshold for a single day during that window, the application is refused. UKVI categorically rejects evidence from cryptocurrency wallets, pension funds, non-liquid investments, and unregulated financial institutions. The chapter maps the exact timing calculation, the £1,529/month London versus £1,171/month outside-London thresholds, the £29,000 spouse visa income requirement, the savings formula for meeting it without employment income, and who can legally provide third-party funds — because using a sibling's or uncle's account instead of a parent's is an automatic refusal that no amount of money can fix.

Germany — Blocked Accounts, Buffer Amounts, and Provider Selection (Chapter 4)

The Sperrkonto system is straightforward in concept — deposit €11,904, receive €992 per month upon arrival — but applicants fail it regularly by transferring the exact minimum amount. International wire transfers lose €50-€200 to intermediary bank fees, and if the final balance lands at €11,850 instead of €11,904, the provider cannot issue the Sperrbescheinigung and your visa application is dead. The chapter covers the recommended buffer, provider comparison (Expatrio, Fintiba, Coracle, Deutsche Bank), the Opportunity Card's higher €1,091/month requirement, and the Verpflichtungserklärung alternative for applicants with a German host.

Australia — Genuine Student Assessment and Source of Wealth (Chapter 5)

Australia's 2024 shift from Genuine Temporary Entrant to Genuine Student changed the financial assessment from "can you pay" to "are you real." Officers now conduct unannounced verification calls to banks in India, Pakistan, and Nepal to confirm that the funds on your statements actually exist. The $29,710 annual living cost requirement plus tuition plus return airfare means a single student often needs to show $50,000-$70,000 AUD in accessible funds. The chapter covers acceptable evidence types, the education loan sanction letter route, the household income alternative ($87,856 AUD for single applicants), and the Subclass 188 business streams where source-of-wealth audits trace every dollar back to its origin.

United States — The I-864 Affidavit and Consular Scrutiny (Chapter 6)

The US system shifts the financial burden from applicant to sponsor through the I-864 Affidavit of Support — a legally binding contract where the sponsor agrees to maintain the immigrant at 125% of the Federal Poverty Guidelines until they become a citizen or accumulate 40 work quarters. The math is deceptively complex: household size includes the sponsor, their dependents, anyone they've previously sponsored with an active obligation, and the new immigrant. The chapter covers the income thresholds, the asset calculation (3x the shortfall for spouse/child of citizen, 5x for other relatives), joint sponsor requirements, and the technical errors on the I-864 that are among the most common reasons for permanent residence denials — mismatched income figures, wrong tax year, digital signatures at posts that require wet ink.

Practical Tools

Red Flags and Fund Parking (Chapter 7)

How immigration officers detect suspicious financial patterns — and how to proactively address them. The five categories of documentation triggers that cause officers to escalate a file for additional scrutiny: fund parking patterns, borrowed funds with round-number transfers from multiple sources, dormant accounts with high balances but no spending activity, income-to-balance mismatches, and format issues like online printouts without URL footers or statements older than 30 days. For each red flag, the guide provides the explanation strategy that converts a suspicious pattern into a documented, verifiable transfer.

Source of Funds Documentation Templates (Chapter 8)

Ready-to-customize templates for the documents that explain legitimate deposits: gift deed affidavits establishing the relationship, amount, and unconditional nature of a transfer. Property sale narratives linking the deed to the bank deposit. Asset liquidation chains showing the path from investment account to liquid savings. Inheritance documentation assembling death certificates, succession certificates, and distribution statements. Plus guidance on writing effective Letters of Explanation — short, specific, supported by evidence, and professional in tone.

Bank Statement Technical Requirements (Chapter 9)

The gap between what your bank considers a "standard statement" and what an immigration officer considers "verifiable evidence." Electronic record-keeping requirements. The URL footer that officers look for on e-statements to verify they were downloaded from the bank's portal rather than edited locally. The physical stamp and branch manager signature that consulates in India, Nigeria, and Pakistan require. Which banks produce compliant statements by default and which ones need a specific request. How to request the exact letter format that IRCC, UKVI, and DHA accept — because "please print my bank statement" and "please issue an official verification letter with average balance, outstanding debts, and institutional contact details on letterhead" produce very different documents.

Financial Readiness Timeline (Chapter 10)

A month-by-month financial preparation timeline keyed to your application date. When to consolidate funds into a single account (six months before). When to stop making large transfers that could trigger pattern flags (three months before). When to request official bank letters (within the country-specific window). How to calculate the exchange rate buffer — because if your home currency devalues 8% during processing, your balance can drop below the threshold in the officer's converted calculation. The recommended 15% buffer and why it protects you from both exchange rate fluctuations and intermediary bank fees.

Multi-Country Comparison Matrix (Chapter 11)

Side-by-side comparison tables for applicants choosing between destinations or applying to multiple countries simultaneously. Student visa requirements and settlement/family visa requirements compared across all five countries — minimum amounts, holding periods, statement freshness windows, locked instruments, sponsor rules, and verification practices — so you can see at a glance which system is strictest, which is cheapest, and which offers the most flexibility in evidence types.

Who This Guide Is For

This guide is for anyone assembling financial documentation for a visa or immigration application who:

- Has the funds but hasn't assembled the proof yet — and doesn't want to discover at refusal that their bank statement format, timing, or account type wasn't compliant with their destination country's specific requirements

- Was refused for "insufficient financial proof" despite having enough money — and needs to understand exactly what went wrong before spending another round of application fees on the same documentation that already failed

- Is applying to Canada, the UK, Germany, Australia, the US, or Schengen countries — and wants the country-specific rules for their destination, not generic advice that conflates Canadian settlement fund requirements with UK maintenance thresholds

- Is using family sponsorship or third-party funds — and needs to navigate the affidavit of support calculations, gift deed requirements, or parent-account rules that govern whose money counts and whose doesn't

- Has legitimate funds with an irregular transaction pattern — a property sale, inheritance, business liquidation, or family gift that created a large deposit needing proper sourcing documentation to avoid a fund parking flag

- Can't afford $500-$1,500 for a document review consultant but needs more than 30 hours of contradictory Reddit threads and outdated YouTube videos to feel confident their financial evidence will pass

Why Not Free Resources?

Free proof of funds advice exists everywhere. Here's what it actually gives you:

- Government websites publish the threshold number — $15,263 for a single Express Entry applicant, €11,904 for a German blocked account. What they don't publish is the format the bank letter must follow, the timing window for when the balance must be maintained, or the transaction patterns that trigger a fraud review even when the money is legitimate. The number is the easiest part. The documentation that proves the number is where applications fail.

- Reddit threads provide real applicant experiences — "I showed six months of statements and got approved" next to "I showed six months of statements and got refused." Without understanding the country-specific rules that differentiate those outcomes, you can't tell which experience applies to your situation. Was the approved applicant in Canada (where six months is standard) or the UK (where the 28-day window matters more than six months of history)? The thread never says.

- YouTube videos from 2023 and 2024 quote thresholds that have since been updated — Canada's settlement funds increase annually, the UK jumped from £18,600 to £29,000 for spouse visas, Australia raised living costs to $29,710. A video recorded before the update gives you the confidence to submit documentation that's below the current minimum.

- Immigration lawyer blogs provide excellent country-specific guidance for the jurisdictions they practice in. They don't cover the country you're not applying to — which matters if you're comparing destinations or if your application involves funds held in a different country's banking system. And a consultation to review your specific documents runs $300-$500 per hour.

- Bank and GIC providers (Expatrio, Fintiba, CIBC) explain their own products clearly. They don't cover how their product fits into the broader financial evidence package, how to handle the remaining funds that aren't in the blocked account or GIC, or what happens if you also need an I-864 or a UK maintenance calculation alongside it.

This guide fills the compliance gap — the space between "I have enough money" and "my documentation proves it in the exact format, timing, and sourcing narrative that this specific country's officers are trained to accept." That's the gap between approval and refusal.

— Less Than One Percent of What's Already at Stake

Document review consultants charge $500-$1,500 to audit your financial evidence. Immigration lawyers charge $300-$500 per hour to review your proof of funds package. These services exist because the stakes justify the cost — a refusal for insufficient financial documentation doesn't just lose the fees you've already paid. It creates a negative record in the immigration database that follows every future application you make, potentially for years.

Your application fees, language tests, medical exams, credential evaluations, and document translations have already cost you $2,700 to $11,400 — often your family's savings, not just yours. The financial documentation is the last component, and it's the one where a formatting error, a timing miscalculation, or an unexplained deposit can invalidate everything that came before it. This guide costs less than the bank letter fee you'll pay to get your statements notarized, and covers the country-specific compliance framework that document review clients pay hundreds of dollars to receive.

30-day money-back guarantee. If the Forensic Compliance System, country-by-country requirements, and red flag toolkit don't strengthen your financial documentation, you get a full refund. No questions.

Download the free Quick-Start Checklist to run a document readiness audit on your current financial evidence tonight. When you're ready for the full Forensic Compliance System — country-specific requirements, red flag toolkit, statement formatting guides, timing calculations, and sourcing templates — the complete guide is here.

You've already saved the money and paid the fees. Don't let a documentation technicality turn a qualified application into a refusal. Prove what you have, the way the officer needs to see it.