You Qualify for Portugal's D7 Visa on Pension Income Alone. What You Don't Know Is That the NHR Tax Exemption on Pensions No Longer Exists, That Your Pension Will Be Taxed at Progressive Rates Up to 48%, That Landlords Routinely Refuse to Register Leases — Silently Disqualifying Your Application, That AIMA Takes 12 to 18 Months to Issue Your Residence Card, That the Citizenship Timeline Just Doubled From 5 Years to 10, and That Your Residency Clock Doesn't Start Until the Physical Card Arrives — Not When You Apply.

You have the pension. You have the savings. You have spent months — maybe years — imagining a life in Portugal where your retirement income stretches further, the healthcare is accessible, and the worst thing that happens on a Tuesday is choosing between the Algarve and the Silver Coast for lunch. You are ready to apply for the D7 Passive Income Visa.

What you are not ready for is what the government websites leave out.

The Portuguese consulate will tell you that D7 applicants need proof of passive income, a criminal record certificate, health insurance, and a housing contract. They will not tell you that the Non-Habitual Resident tax regime — the flat 10% rate on foreign pensions that made Portugal famous among retirees — closed to new applicants in April 2025, and its replacement, IFICI, explicitly excludes pension income from any preferential treatment. They will not explain that most Portuguese landlords refuse to register rental contracts with the tax authority to avoid paying 25% income tax on the rent, and that an unregistered lease is invisible to immigration authorities — meaning your €1,200-a-month apartment does not count as proof of accommodation. They will not mention that AIMA, the agency that issues your residence card, is running a 12-to-18-month backlog for first cards, or that during this wait your ability to travel within Europe is severely restricted. And they will not warn you that in May 2026, the path to Portuguese citizenship was doubled from 5 years to 10, with the residency clock now starting from the date your physical card is issued — not the date you applied — adding up to 18 months of dead time to what is already a decade-long commitment.

Reddit gives you fragments. One retiree approved in eight weeks, another waiting fourteen months with no AIMA appointment. Someone says bank savings alone are sufficient. Someone else was rejected because their consulate demanded twelve months of recurring deposits, not a lump sum. A post from 2023 promises a flat 10% tax on your UK pension. That post will get your tax planning catastrophically wrong in 2026. The free information is real — it is also contradictory, outdated, and incomplete in exactly the ways that cause rejections, tax surprises, and months of preventable limbo.

This is the reality every D7 applicant in 2026 discovers: the visa application is the easy part. The hard part is what happens after — the tax shock when your pension is assessed at 25% to 35% instead of the 10% you expected, the lease that turns out to be unregistered, the AIMA backlog that traps you in Portugal without a residence card, and the citizenship timeline that is no longer 5 years but closer to 12 once you account for processing delays.

The Portugal D7 Passive Income Visa Guide is a Post-NHR Tax Reality Blueprint built for the specific challenge retirees and passive income earners face in 2026: converting qualifying income into an approved D7 visa, navigating the bureaucratic infrastructure that no government website describes accurately, and building a financial foundation that survives the end of preferential pension taxation. This is not a summary of the AIMA website. This is the integrated system covering the 2026 income thresholds with proof strategies for pension recipients, dividend earners, rental income holders, and mixed-income applicants, the D7 vs D8 decision framework that prevents you from filing the wrong visa type, the complete document checklist with apostille requirements and validity windows calibrated to the zero-tolerance rule, the Lease Trap and how the August 2025 tenant self-registration law solves it, the post-NHR tax reality with worked examples at every income level, the healthcare sequencing from private insurance through SNS registration, the AIMA backlog survival manual with the Article 66 legal remedy, the May 2026 citizenship law impact, and the region-by-region cost of living breakdown for Lisbon, Porto, the Algarve, the Silver Coast, and the interior.

What's Inside the Post-NHR Tax Reality Blueprint

The complete 67-page guide, a quick-start checklist, and eight standalone printable tools — covering every step from income verification through permanent residency:

The D7 vs D8 Decision Framework

If you have a pension and nothing else, you are D7. But the moment you add consulting income, a remote freelance project, or fees from a side business, the line blurs — and consulates in 2026 enforce the distinction between passive and active income with no tolerance for ambiguity. Filing D8 when your income is primarily passive wastes money on the higher €3,680/month threshold. Filing D7 when you have meaningful active income gets your application rejected. The guide provides the decision matrix for pure pension income, pure investment income, mixed passive-and-active income, and the gray zone where you earn dividends from a company you also manage — with the specific evidence strategy that keeps your D7 classification defensible under consular scrutiny.

The Income Proof Strategies for Every Passive Source

The D7 requires €920 per month (€11,040 annually) from non-Portuguese passive sources. But "proof" means different things depending on how you earn. Pension recipients need official benefit letters from Social Security, the UK State Pension Service, or their national equivalent — self-generated summaries are rejected. Dividend earners need brokerage statements showing 12 months of consistent distributions, not a portfolio value screenshot. Rental income holders need signed lease agreements and matching bank deposits, not a letter from a property manager. The guide covers each income pathway with the documents consulates actually accept, the evidence gaps that trigger rejections, the "savings buffer" that most consulates expect beyond the minimum (typically 12 months at €11,040), and the family multiplier calculations: €1,380 for couples, €1,656 with one child, €1,932 with two — with specific strategies for when only one spouse has qualifying income and the other must apply as a dependent or later through family reunification.

The Lease Trap and How to Defeat It

Thousands of D7 applications have been rejected or delayed because of unregistered leases. Here is how the trap works: you find an apartment, sign a 12-month contract, pay three months upfront plus a security deposit — often €3,000 to €5,000 in Lisbon or the Algarve. Your landlord does not register the lease with the Finanças (tax authority) because registration triggers a 25% tax on rental income. Without the registration receipt (Modelo 2), your lease is invisible to immigration authorities. The consulate or AIMA sees no proof of accommodation. Your application stalls or is rejected, and your deposit is locked in a property you cannot use for visa purposes. The guide covers how to verify registration status before signing, the specific clause to include in your contract that requires the landlord to register, and — critically — the August 2025 law that allows tenants to self-register their lease if the landlord refuses, bypassing the single most common cause of D7 application failure in 2026.

The Post-NHR Tax Reality

This is the section that saves retirees the most money — or at least prevents the shock that derails their financial planning. The Non-Habitual Resident regime offered a flat 10% tax on foreign pensions. It is gone. The replacement, IFICI (sometimes called NHR 2.0), retains a 20% flat rate but restricts eligibility to five professional sectors: IT, engineering, healthcare, certified startups, and finance. Pension income does not qualify. Period. As a standard Portuguese tax resident, your worldwide income — pensions, dividends, interest, rental income — will be taxed at progressive rates from 12.5% on the first €8,342 to 48% on income above €86,634, plus a solidarity surcharge for high earners. The guide provides worked tax calculations at five income levels (€15,000, €25,000, €40,000, €60,000, and €100,000), covers the specific treatment of US Social Security (taxable primarily in the US under the treaty), UK State Pension (taxable only in Portugal), Canadian CPP/OAS (subject to treaty reduction), and the Roth IRA trap — Portugal does not recognize Roth tax-free status and may tax the growth portion of withdrawals as pension income. It also covers the "net disposable income" comparison that shows why Portugal remains financially attractive for most retirees despite higher taxes, because the total cost of living — healthcare, housing, food, transportation — is 40% to 50% lower than the US, UK, or Canada.

The Pre-Application Infrastructure Sequence

Before you can apply for the D7, you need three things that depend on each other in a specific order. The NIF (Portuguese tax number) requires appointing a fiscal representative at €150 to €400 per year. The Portuguese bank account requires a NIF. The registered lease requires a bank account for deposits and a NIF for the tax registration. Start this sequence in the wrong order and you lose months. The guide maps the exact dependencies, provides the timeline for each step (NIF: 1 to 3 weeks via ePortugal, bank account: 2 to 6 weeks depending on whether you can open remotely via video call, lease: varies), covers which banks accept remote account opening for non-residents, and explains how to negotiate with landlords on registration — including the leverage points that make registration in their interest, not just yours.

The Zero-Tolerance Document Checklist

Since April 2025, AIMA enforces a "complete application" policy: if any document is missing, expired, or improperly authenticated at the time of your appointment, the case is closed. No requests for additional documents. No grace period. The guide provides the complete checklist with validity windows reverse-engineered from typical processing times — so your criminal record certificate (90-day expiry) does not expire while your consulate takes 60 to 90 days to process. It covers apostille requirements for Hague Convention countries, the full legalization chain for non-Hague countries, certified translation standards (Portuguese translators only — translations from your home country are not accepted), and the specific document format each major consulate expects, including the consulate-specific requirements at VFS centers in Miami, San Francisco, London, and Toronto.

The AIMA Backlog Survival Manual

You arrive in Portugal on your D7 entry visa. Your AIMA biometrics appointment could be three months away or nine months away. In the meantime, you need healthcare, banking, and the ability to travel. The guide covers what your legal status actually is during the wait (you are legally resident, but only within Portugal), how to register at your local Centro de Saude for public healthcare access once your card arrives, why you must maintain private insurance during the entire wait period, and the Direct Entry Rule — the only safe way to travel internationally while your residence card is pending. The rule: fly directly between Portugal and non-Schengen countries only. Do not transit through Spain, France, Germany, or any other Schengen country. Border agents in those countries may not recognize your AIMA extension documents, and the consequences — detention, deportation, a five-year Schengen ban — are not theoretical. The guide also covers the legal remedy of suing AIMA for administrative silence under Article 66 of the CPTA, which typically produces a court-ordered appointment within 8 to 10 weeks at a cost of approximately €1,000 in legal fees.

The Healthcare Bridge

For retirees, healthcare is not a line item — it is the reason many are considering Portugal in the first place. But the sequencing matters. D7 holders are eligible for Portugal's public health service (SNS) only after they receive their residence card and register at their local Centro de Saude. Until then — which means during the entire 12-to-18-month AIMA wait — you rely on private insurance. The guide covers the minimum coverage required for the visa application (€30,000 including hospitalization and repatriation), the transition from travel insurance to residency-compatible private insurance, the SNS registration process once your card arrives, the "hybrid coverage" strategy most experienced expats use (SNS for subsidized prescriptions and chronic care, private insurance for specialist access and avoiding 18-month surgery wait lists), and comparative healthcare costs: a GP visit at €5 through SNS versus €50 to €70 private, a specialist at €7 versus €90 to €150, an ER visit at minimal cost versus €400 private.

The May 2026 Citizenship Law Impact

On May 3, 2026, the Portuguese president signed a revised nationality law that changed the long-term calculus for every D7 holder. The standard residency requirement for naturalization increased from 5 years to 10 years for non-EU, non-CPLP nationals. EU and CPLP citizens saw their requirement increase from 5 to 7 years. And the residency clock reversal means your time no longer counts from the date you applied for your residence permit — it counts from the date the physical card is issued. Given AIMA's processing times, this adds 12 to 18 months of dead time to the statutory 10-year requirement, making the realistic path to a Portuguese passport 12 to 13 years. The guide covers what this means for your planning, why permanent residency at 5 years remains unchanged and may be the more practical goal for most retirees, how the A2 Portuguese language requirement works (and when to start studying), and the new civic knowledge test that applies to all naturalization applicants.

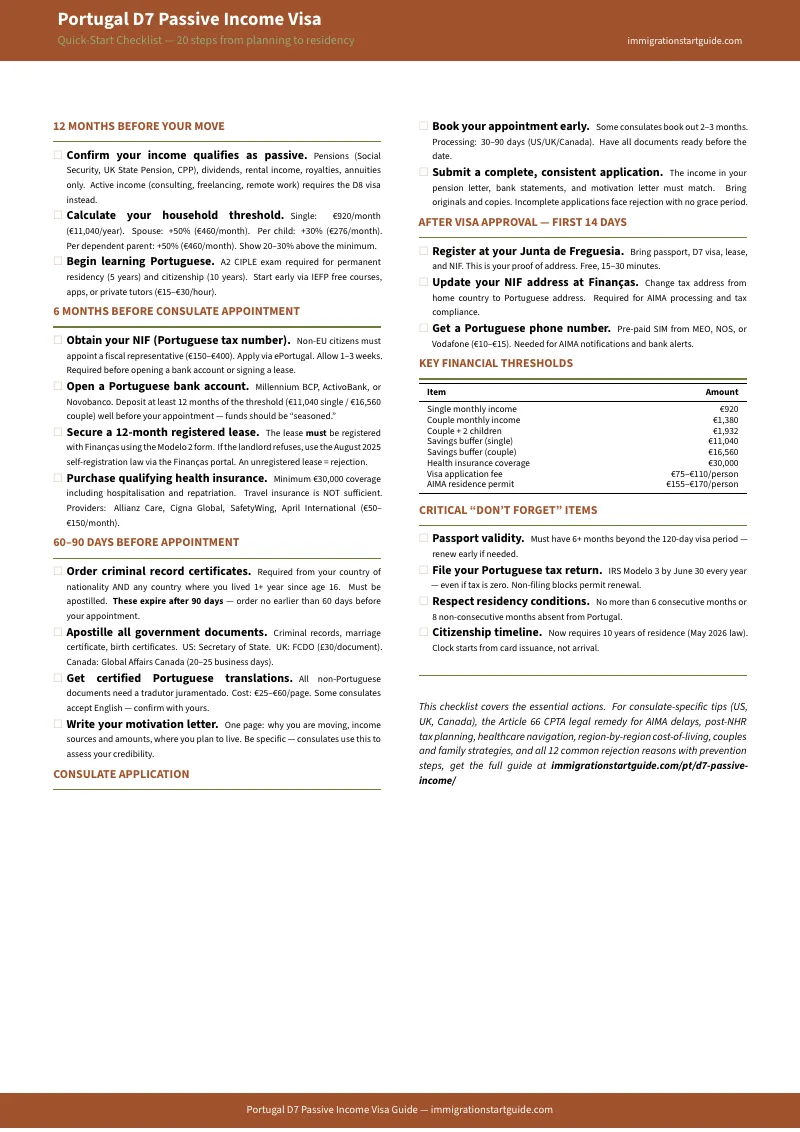

Quick-Start Checklist (free download)

The critical steps distilled into a single action sheet organized by phase: income type confirmation and D7 vs D8 classification, pre-application infrastructure setup (NIF, bank account, registered lease), consulate submission with the zero-tolerance document list, post-arrival first 30 days (address registration, AIMA biometrics, private insurance maintenance), and the waiting period survival rules. Enough to audit your situation tonight and identify whether your income qualifies, which documents you are missing, and where the Lease Trap could catch you.

Eight Standalone Printable Tools

In addition to the full guide and checklist, you get eight reference tools you can print and use independently — at your desk while gathering documents, at your consulate appointment, and on your fridge in Portugal while waiting for your AIMA card:

- D7 vs D8 Decision Matrix — one-page comparison with an income scenario decision table

- Income Proof Reference Card — what documents each passive income type requires

- Zero-Tolerance Document Checklist — every document with apostille requirements and validity windows

- Tax Calculation Worksheet — progressive tax rates, worked examples, and a blank personal calculator

- Pre-Application Timeline — the NIF → bank → lease dependency chain with a fillable date tracker

- AIMA Backlog Survival Card — the Direct Entry Rule, healthcare access, and Article 66 remedy

- Regional Cost-of-Living Comparison — six regions compared side-by-side

- Rejection Prevention Checklist — 12 common rejection reasons as a pre-submission audit

Who This Guide Is For

This guide is for retirees and passive income earners who want to live legally in Portugal on the D7 Passive Income Visa:

- US retirees living on Social Security and private pensions who need to understand the post-NHR tax reality — your pension will be taxed in Portugal at progressive rates, not the flat 10% you read about in 2023 articles, and the guide provides worked examples at your income level so you know the actual number before you commit to the move.

- UK pensioners considering Portugal after Brexit restricted free movement — the D7 is your pathway back into Europe, but the UK State Pension is now taxable only in Portugal under the double taxation agreement, and the guide covers exactly what that means for your effective rate at every income bracket.

- Canadian retirees on CPP and OAS who need the treaty-specific guidance on source-country withholding — Canada applies a 25% non-resident tax that the treaty can reduce to 15%, and the guide walks through the specific forms and timing to claim the reduction before you lose money to double taxation.

- FIRE community members in their 30s to 50s living on dividend portfolios, rental income, or systematic withdrawal strategies — the guide covers how to present the "4% rule" as qualifying passive income, the documentation that proves recurring dividends to a consulate that expects traditional pension letters, and the D7 vs D8 decision for those who also do occasional consulting.

- Couples where one partner has strong pension income and the other has little or none — the guide covers the dependent application process, the family multiplier calculations (€1,380/month for couples), and the specific evidence requirements when one spouse's income must support both applications.

- Property investors and landlords who earn rental income from multiple countries — the guide covers how to document geographically distributed rental income as a coherent proof package, the tax treatment of foreign rental income under Portuguese progressive rates, and the foreign tax credit mechanics that prevent double taxation.

This guide is not for: Remote workers earning primarily from active employment or freelancing (see the Portugal D8 Digital Nomad Visa Guide), applicants seeking Portuguese citizenship through ancestry, marriage, or Sephardic heritage (see the Portugal Citizenship Guide), or Golden Visa applicants investing €500,000+ in qualifying funds.

Why Not Free Resources?

Free information on the D7 visa exists across government portals, expat forums, YouTube channels, and law firm blogs. Here is what it actually delivers:

- The AIMA website and ePortugal list the requirements: passive income, criminal record, health insurance, housing proof. They do not explain the Lease Trap, the post-NHR tax rates on pensions, the savings buffer most consulates expect beyond the legal minimum, the healthcare sequencing from private insurance through SNS registration, or the zero-tolerance document policy that took effect in April 2025. The government tells you what to submit. It does not tell you how to survive the 12-to-18-month gap between submission and card issuance, or what your tax bill will actually look like.

- Reddit and Facebook groups give you anecdotes. One retiree approved in six weeks. Another rejected because their consulate demanded recurring monthly deposits, not savings. A third who moved based on 10% NHR pension taxation and discovered a 25% effective rate on arrival. Each story is real. None tells you which scenario applies to your consulate, your income type, or your nationality. You leave the forum more confused than when you arrived — and with no way to distinguish the advice of someone who applied in 2022 from someone who applied last month.

- YouTube channels and blog posts were mostly created when NHR still existed or when the citizenship requirement was 5 years. A video titled "Retire to Portugal Tax-Free" that references the 10% pension rate or promises a European passport in 5 years will get your financial planning and your long-term expectations catastrophically wrong in 2026. The content creators have not updated because the algorithm rewards new videos, not corrections to old ones.

- Amazon books retail for $15 to $25 and were written months before publication. The most popular Portugal retirement books reference income thresholds from 2024 (before the minimum wage increase to €920), the NHR regime (closed April 2025), and the 5-year citizenship path (doubled to 10 years in May 2026). A book that costs $20 and gives you outdated tax rates costs you far more than $20 when you build your retirement budget around the wrong numbers.

- Immigration lawyers and relocation consultants charge €2,000 to €10,000 for full D7 service. They handle the filing. They do not teach you how to evaluate your post-NHR tax position, choose between Lisbon and the Algarve based on healthcare infrastructure, survive the AIMA backlog, plan for the 10-year citizenship timeline, or navigate the healthcare transition from private insurance to SNS. Their fee covers the application. Your financial planning, your healthcare strategy, and your post-arrival survival are your problem — and those are the parts where most retirees make the expensive mistakes.

This guide fills the gap between "I know I want to retire in Portugal" and "I have my residence card, my tax filing is correct, my healthcare is sorted, and I know exactly what to expect for the next 10 years" — the space where qualified applicants still fail because they assumed NHR still existed, trusted an unregistered lease, miscalculated their tax exposure, or discovered the AIMA backlog travel restrictions after booking a connecting flight through Madrid.

— Less Than One Certified Translation

An immigration lawyer charges €2,000 to €10,000 for a standard D7 filing. A relocation consultant charges €300 to €500 just to set up your NIF and fiscal representative. A single rejected application costs you the non-refundable consulate fee (€75 to €110) plus three to six months of delay while you gather corrected documents and reapply. A lease that turns out to be unregistered costs you your housing deposit — €3,000 to €5,000 in Lisbon or the Algarve — plus the time to find a new apartment with a compliant landlord. A tax plan built on NHR rates that no longer exist costs you thousands in the first year when your actual bill arrives.

This guide costs less than a single certified translation of a birth certificate and covers every step, every document, every tax calculation, and every post-arrival survival strategy between your first NIF application and your permanent residence card. The Lease Trap section alone can save you from the most common cause of D7 application failure in 2026. The post-NHR tax analysis can save you from building your entire retirement budget on numbers that are two years out of date.

You have the income. You have the savings. Portugal has the visa. What stands between you and a legal retirement in Europe is not qualification — it is execution. The zero-tolerance rule means there are no practice runs. The AIMA backlog means you cannot afford to waste months on a rejected first attempt. The May 2026 citizenship law means every month of delay adds to what is now a 12-to-13-year path to a European passport — or, more practically, an 11-to-12-year wait that ends with the permanent residency card that most retirees will find sufficient.

30-day money-back guarantee. If the income proof strategies, the Lease Trap prevention, the post-NHR tax calculations, the document checklist, and the AIMA survival manual do not make your application stronger than anything you could assemble from Reddit threads and 2023 YouTube videos, you pay nothing.

Download the free Quick-Start Checklist to confirm your D7 eligibility, verify your income type, and identify whether the Lease Trap or the tax changes affect your situation. When you are ready for the complete Post-NHR Tax Reality Blueprint — the full guide with income proof strategies for every passive source, the Lease Trap solution, the zero-tolerance document checklist, the worked tax calculations at your income level, the healthcare bridge strategy, the AIMA survival manual, and the 10-year citizenship roadmap — the full guide is here.

Your pension qualifies. Your savings are sufficient. Now build the application that gets approved on the first attempt — in a system that no longer gives you a second one.